Document_GEM: Monthly Briefing on the World Economic Situation and Prospects

Monthly Briefing on the World Economic Situation and Prospects

14 April 2025

Geopolitical fragmentation, trade barriers, and climate change portend recurrent supply-side shocks, fuelling unpredictable inflationary pressures. These disruptions are increasing uncertainty and volatility, which complicate investment decisions and economic policymaking.

6 March 2025

The near-term global trade outlook is fraught with uncertainties amid new tariffs and other trade restrictions. While recent history demonstrates that the global trading system is resilient, often adapting by finding alternative channels for sustaining commerce, policy uncertainty could hinder this process by discouraging necessary investments.

3 February 2025

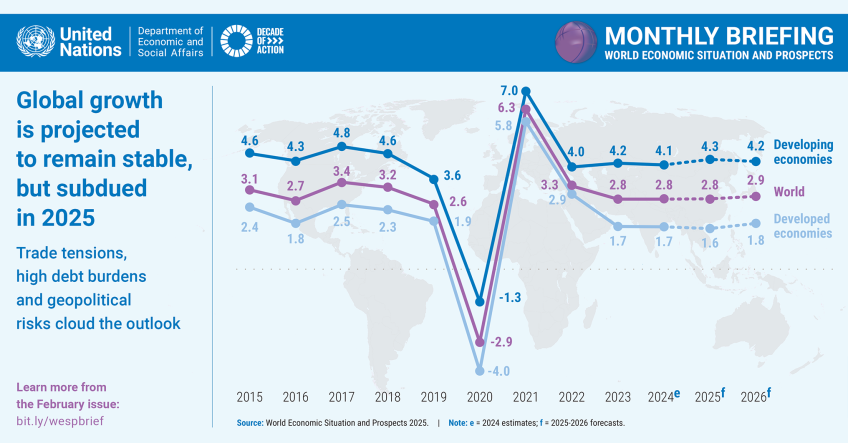

The world economy has shown resilience despite multiple shocks, but the outlook remains uncertain due to ongoing conflicts, geopolitical and trade tensions, climate risks, and mounting fiscal pressures.

1 November 2024

Economic growth in landlocked developing countries (LLDCs) is expected to be steady in the near term but remains well below the average in the pre-pandemic decade. Substantial downside risks remain, including commodity price volatility, debt challenges, climate disasters and geopolitical tensions.

1 October 2024

The global automotive market is experiencing transformative shifts, with China emerging as a leading force in electric vehicle (EV) production and exports. In contrast, traditional powerhouses like Germany, Japan, the Republic of Korea, and the United States are facing stiff competitiveness challenges.

3 September 2024

Monetary policy, implemented through changing interest rates, can lead to gender differentiated impacts on work, income and consumption, savings, wealth, and asset ownership.

7 August 2024

About 20 years ago, eight Eastern European countries joined the European Union. EU membership facilitated economic growth, transfer of new technology and knowledge to these countries, leading to the modernization and diversification of their production and export base.

2 July 2024

Climate change has emerged as a source of supply shocks and a key risk to the global economy. While localized supply shocks may have a limited impact, multiple severe events – such as those associated with climate change- can push inflation up.

3 June 2024

The majority of central banks kept their policy rates unchanged in the first quarter of 2024, closely watching the decisions of the United States Federal Reserve and the European Central Bank.

Follow Us